Cracks in Reality

"But he felt a deep foreboding that despite all the good around him and perhaps even somewhere within it there still resided something morbid."

– Fyodor Dostoevsky

Over the past two weeks, I’ve reached the same conclusion of many individuals and the collective consciousness we call the stock market: We are likely in the beginning stages of a financial crisis that could rival the Great Depression.

Canary in the Coal Mine

I’ll leave the news coverage to the experts, who dig into this in far more detail. Particularly, Matt Levine has the best explanation I’ve seen of the mechanics of the Silicon Valley Bank failure.

In summary:

-

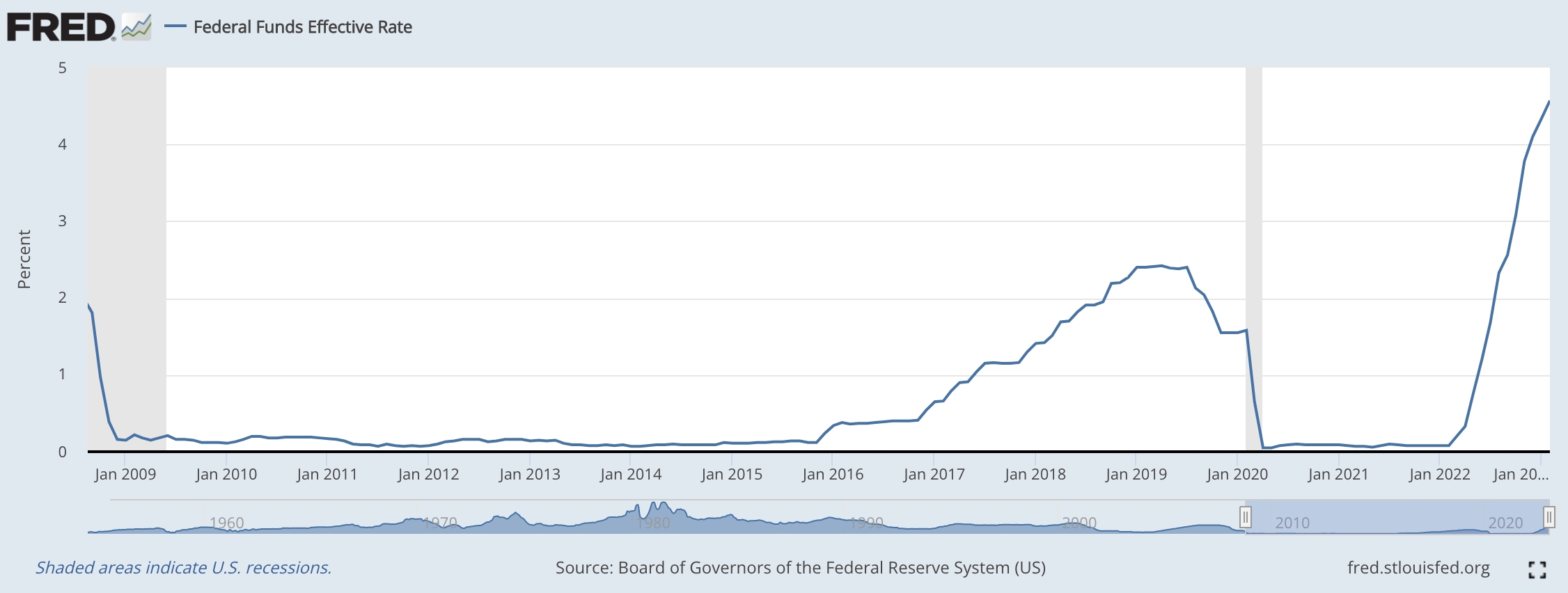

The Fed printed a ton of money over the past few years, after a decade of historically low interest rates.

-

Much of that money flowed into startups and tech companies, who parked it at Silicon Valley Bank.

-

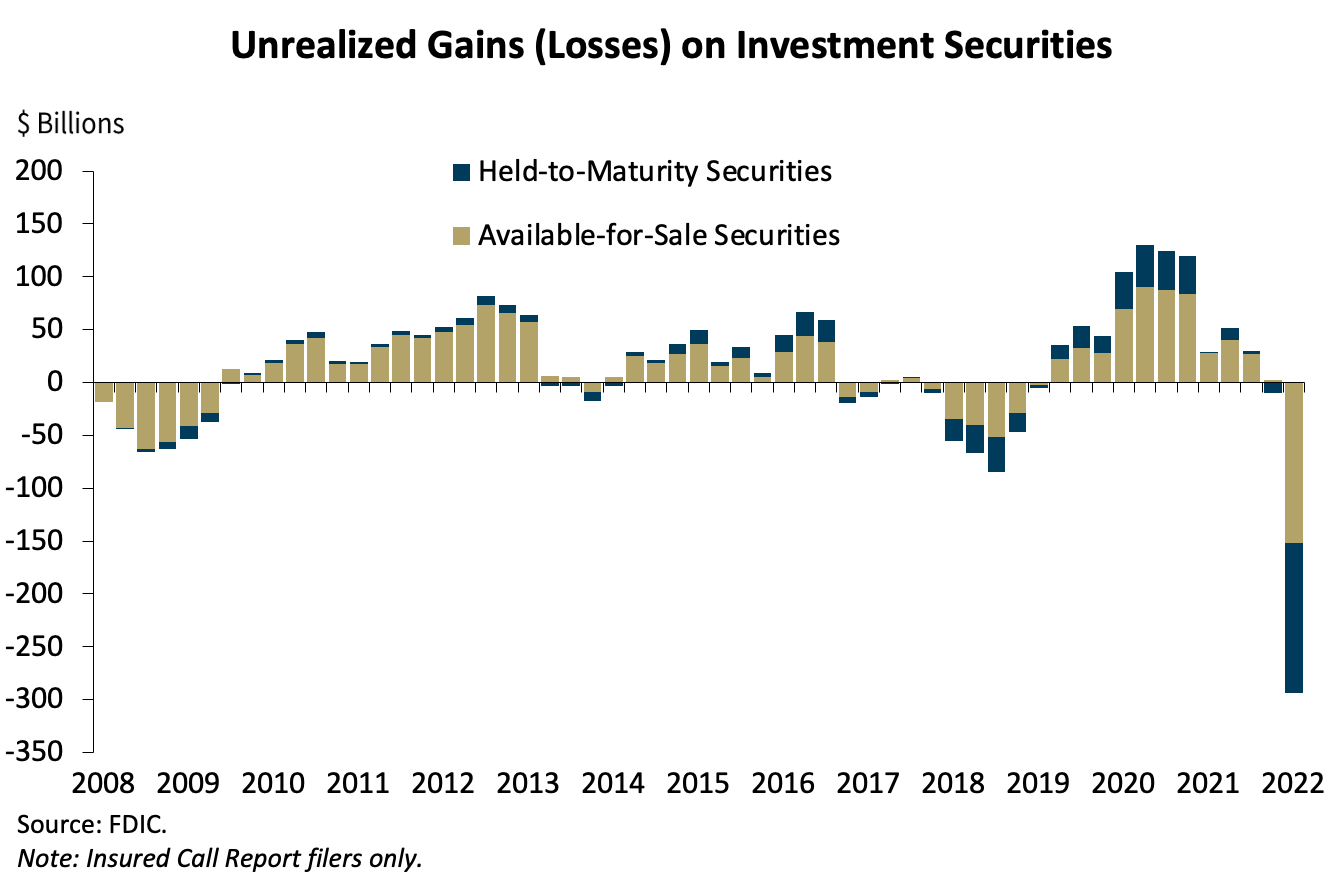

Silicon Valley Bank, sitting on a huge pile of cash, put it into “safe” investments: US Treasuries and agency mortgage-backed securities.[1]

-

Silicon Valley Bank invested this money into long-term bonds. The risk management team at Silicon Valley Bank…wasn’t great, as it appears to have not taken into account duration risk.

-

The Fed raised interest rates from ~0% to ~5% in the span of a year.

-

The investments that Silicon Valley Bank made were then underwater.[2]

-

Customers realized this and started to withdraw their funds, triggering a full-on bank run.

-

Arrivederci Silicon Valley Bank. Bonjuorno FDIC.

This happened extremely quickly. On March 9, 2023, Silicon Valley Bank depositors attempted to withdraw $42 billion. The bank run was triggered by triggered by Silicon Valley Bank’s extremely online customer set: startup founders and venture capitalists. For all of their talk of being contrarian, there may be no more interconnected and lemming-like group than VCs.

The narrative in some camps is already that tech companies and VCs are the baddies. This is the exact same thing we saw in the ’08 Financial Crisis: the vilification of the financial industry. We need a scapegoat.

But this can happen to any bank.

Reflexivity: Or, the Financial Industry Is Our Economy

Patrick MacKenzie has the best explanation of what this means for the broader banking system. An important point, buried at the end of the essay, is:

“I live in a society, which is sufficient information for you to know that I’m structurally levered long to the stability of the banking system, much like you are.”

We are all dependent on our financial system. As software eats the world, our work becomes increasingly interconnected. A couple of regional banks failing may not matter to you — unless you realize that your payroll provider used one of those banks, so your paycheck won’t come through this week. Or you’re a small business owner, and someone you’ve invoiced has all of their funds tied up in a failed bank. Oops! Better write off that line item in your accounts receivable.

Back in the halcyon days of 2020 and 2021, as the COVID money printer went brrr, many people took out loans to buy houses at a 2% interest rate. Yes, banks have risk management departments. They can conduct all sorts of financial voodoo — hedge their exposure with swaps, slice and dice the loans into derivatives and sell them to another institution, etc. But those loans now yield less than Treasuries and the underlying asset value has declined significantly. And at the end of the day they are stuck on someone’s balance sheet.

So this sort of thing matters to Joe Sixpack, whether or not he is aware of it. And in 2023 (contrasted with 2008) we are increasingly online and interconnected. One bad earnings report can trigger a run on the bank. Perception drives reality and reality drives perception in a recursive loop. Our entire economy is just a colossal, scaly ouroboros.

Every Finance 101 class should be renamed “History of Finance”. A modern finance class should demonstrate that we are not rational actors in an efficient market, but that sentiment drives financial fundamentals reflexively. As I’ve written previously,

Reflexivity is the idea that our perception of circumstances influences reality, which then further impacts our perception of reality, in a self-reinforcing loop. Specifically, in a financial market, prices are a reflection of traders’ expectations. Those prices then influence traders’ expectations, and so on.

Hell, some claim that one independent newsletter writer could have kicked off this whole thing.[3]

In financial markets and our economy, as in quantum physics, there is an observer effect. This is how we experience a bifurcated existence — we simultaneously have the best job market of the past 50 years and are worried about structural unemployment and hyperinflation.[4]

So the Fed can try to pump more money into the economy, but our economy is already a Saturnalia feast approaching the winter solstice. Maybe we can stuff a few more oysters down our gullet, but it’s only a matter of time before we need to visit the vomitorium.

Reality Cracks

This reflexivity is not limited to financial markets. Soros was a philosopher before he was a trader.

Things have gotten…weird over the past several years. At first, I thought this was a result of my transition to adulthood,[5] and all of this was a part of understanding the complexity of the modern world. But now I’m not so sure.

Others have noticed this:

A forced wind-down of Credit Suisse, a run on US regional banks, the arrest of a former US President, the launch of GPT-4 … I was in the trenches in 2008, and I never felt like system-shattering events were advancing so quickly and (w/exception of GPT-4) on so little substance.

— Ben Hunt (@EpsilonTheory) March 18, 2023

Here's one more for those more conspiratorially-inclined. Recent rate hikes might be an attempt by the Fed to get people to buy Treasuries directly as opposed to keeping their money in banks. This could lead to the government issuing a CBDC and all of the potential spying and censorship inherent in this product.

Far-fetched? A few years ago I would have told you there is no way the people of the U.S. would allow this, given the distrust of government that comprises a large part of the American psyche. But now, I’m not so sure. We’ve already given up any sense of privacy when it comes to financial transactions.

Harari tells us that everything we call life, our entire societal fabric, is made up of shared myths and beliefs. These concepts — democracy, capitalism, religion — lose their power when we stop believing in them.

An acceleration in societal unraveling has been occurring since arguably the 2016 election[6], but COVID in particular led to the cracking of many of our shared myths. Globalization as a force for good. Institutional trust. The stock market reflecting the health of an economy. Reliance on experts to tell the truth. Scientific knowledge.

Yet all of these phenomena are symptoms, not the affliction. We live in the apotheosis of postmodernism, an age where our collective consciousness has become conscious of itself and is throwing off the yoke of the postwar liberal world order.

It doesn’t matter what happens. It matters how we react — and these reactions are filtered through the lens of tribal association.

“Can you believe the Blue Tribe thinks that voter fraud isn’t a huge problem? Really?”

“Wow, glad I don’t associate with anyone in the Red Tribe. They don’t trust science.”

“I’m going to write a 5,000 word blog post to better solidify my place in the Gray Tribe hierarchy.”[7]

We see this play out in every current event. Within a few days of the Silicon Valley Bank crisis, Congress was rushing to control the narrative.

Nihilism as the Defining Philosophy of Our Time

So what can one do? The inevitable consequence of a world that lacks cause-and-effect rules, where the effect drives the cause — perhaps even a rational response to that world — is a collective shrug. And that’s what we’ve done. Nihilism is the defining philosophy of our times.

Nihilism is voting for a billionaire with populist rhetoric because no other politician will deign to lend validity to your problems.

Nihilism is realizing the Unabomber had some pretty good points.

Nihilism is making an 100x return buying shitcoins or trading SPACs and then losing it all.

Nihilism is becoming aware that LLMs — not in the future, but now — are smarter than you and will soon take your job.

Nihilism is understanding that hypergrowth tech companies are largely kayfabe. DoorDash, Uber, and the like may not make any money, but that was never the point. They just needed to convince a few VCs of the narrative of growth.

Nihilism is opting out of our democratic experiment because all politicians do is accumulate money and power while tilting at windmills with the gusto of Don Quixote.

Nihilism is sensing that your gender is superfluous.

Nihilism is publicly stating (joking?) you have a good chance of ending the world with AI and charging ahead with its development anyways.

Nihilism is comprehending all of this, predicting non-negligible odds of some sort of societal upheaval, buying Bitcoin, and then realizing that nuclear powers, not code, enforce property rights. Bullets and food will be the true medium of exchange if the world’s largest nuclear power and issuer of its reserve currency actually fails.

All of these are examples of the same phenomenon. Societal and economic forces have built up inside a pressure cooker that is now boiling over.

Nihilism has been a theme underpinning my writing, from Gamestop mania to war in Ukraine. Our mindset is perhaps best explored by the (outstanding) movie Vengeance.

Everything means everything…so nothing means anything.

I’m falling victim to this exact same mindset — at least in a small way — with this blog post. I need to be relevant. I need to have a unique take. I need to create something that will outlive me. I need to prove how smart I am through some onanistic intellectual exercise, when I should be spending time building a company, connecting with the people in my life, or just…surfing.

What am I even doing here?

What's Next?

The past few years of brrr-ing money printing and remote work boondoggle for the upper-middle class was one last hurrah before a huge economic and societal crisis. A Fourth Turning, if you will.

Last year when reviewing Strauss and Howe’s book, I was skeptical of the claims that generational cycles drive history. I wrote,

“[T]hese are bold forecasts that I suspect overfit to the training data, much more hedgehog than fox.”

But over the past year, I’ve become much more sympathetic to their cyclical views of history. What has changed my mind? The signs were there a year ago, but I’ve recently started paying more attention to:

- Our pace of technological revolution, specifically with regards to AI.

- The rapid deglobalization of the world in the wake of COVID, U.S.-China tensions, and Russia’s invasion of Ukraine.

- The “wacky” economics of the past couple of years and their parallels to the buildup to the Great Depression.

- More conversations I’ve had with individuals from across the political spectrum where I better understand the extent of political polarization and how everyone constructs their own reality and lives in their own filter bubble.

So if our society is currently undergoing a natural “unraveling” that will ultimately result in a society-shaping event at the scale of World War II, my bet would be on AI creating massive unemployment, which would be the necessary catalyst for a new economic paradigm.[8]

That said, that is just a shot in the dark. All I know is that our old myths no longer serve us. We are tearing them down and constructing new ones.

Here, people will be triggered by the phrase mortgage-backed securities. They’ll scream, “We learned nothing from the 2008 Financial Crisis!” But, as Ben Thompson says:

↩︎“Agency” is an important distinction: these weren’t the ugly subprime mortgages that were at the heart of the 2008 financial crisis; these were mortgages ultimately backed by federal mortgage programs.

Bond Pricing 101. The salient fact is that bond prices have an inverse relationship with interest rates. ↩︎

Pretty badass if Byrne can call himself the Gavrilo Princip of a financial crisis. ↩︎

From the aforementioned Byrne Hobart:

↩︎“[W]hat if all this credit and liquidity creation threatens trust in the entire financial system, and leads to faster inflation, or even hyperinflation?…But note that both of the previous episodes led, in the short term, to a drop in inflation: the CPI hit 5% for the first time since the early 90s in 2008, just before the crisis. Banking crises are typically deflationary, so you can use the central bank interventions in their wake as a proxy for how deflationary they are when there isn't a policy response. The Fed added $3.5tr to its balance sheet in the six years following the financial crisis, which was just enough to get inflation from the pre-crisis level of around 3% to the next decade's average of 1.6%. Post-Covid, a $2.9tr in balance sheet expansion was also just enough to keep year-over-year inflation slightly above zero in the first few months of the pandemic."

I graduated from college in 2015. ↩︎

Venkatesh Rao has a whole series on this phenomenon. ↩︎

Tribal definitions here come from Scott Alexander’s excellent piece, I Can Tolerate Anything Except the Outgroup. ↩︎

Of course, this assumes a slow takeoff. In a fast takeoff scenario we’re all dead. ↩︎